Starting financial planning can seem daunting. But it’s essential for a secure future.

Financial planning helps you manage your money wisely. It sets you on the path to achieving your goals. Whether you’re saving for a home, planning a vacation, or preparing for retirement, financial planning is crucial. It involves budgeting, saving, investing, and understanding your expenses.

By taking control of your finances, you can reduce stress and build a stable financial future. This guide will help you grasp the basics and start your financial journey confidently. So, let’s dive in and make financial planning simple and manageable for you.

Credit: www.udemy.com

Introduction To Financial Planning

Starting your financial planning journey can feel daunting. But it is essential. Financial planning helps you manage your money better. It sets you up for a secure future. Understanding basic concepts can make this process easier. Let’s dive into the key components.

Importance Of Financial Planning

Financial planning is crucial for several reasons:

- Security: It ensures you have funds for emergencies.

- Goals: Helps you achieve short-term and long-term goals.

- Debt Management: Allows you to manage and reduce debt.

- Investments: Guides you in making wise investment choices.

- Retirement: Prepares you for a comfortable retirement.

Without a plan, managing finances can be stressful. A financial plan provides clarity. It helps you track your income, expenses, and savings. This clarity leads to better financial decisions.

Common Financial Goals

Everyone has different financial goals. But, some goals are common among beginners:

- Building an Emergency Fund: Save at least three to six months’ worth of expenses.

- Paying Off Debt: Prioritize high-interest debts first.

- Saving for Retirement: Start early to benefit from compound interest.

- Buying a Home: Save for a down payment and closing costs.

- Education Funds: Save for your children’s education or your own further studies.

Setting clear financial goals is vital. It gives you a roadmap. It helps you stay focused and motivated. Regularly reviewing your goals can keep you on track.

| Financial Goal | Recommended Action |

|---|---|

| Emergency Fund | Save 3-6 months of expenses |

| Debt Repayment | Prioritize high-interest debts |

| Retirement Savings | Start early with small contributions |

| Home Purchase | Save for down payment |

| Education Funds | Regular monthly savings |

Remember, financial planning is a continuous process. It evolves with your life stages and circumstances. Stay committed, and your efforts will pay off.

Setting Financial Goals

Setting financial goals is the first step to a healthy financial life. It gives you direction and a clear path to follow. Clear goals help you make informed decisions. They also motivate you to save and invest wisely. Let’s dive into short-term and long-term financial goals.

Short-term Goals

Short-term goals are targets you aim to achieve within a year. These could include saving for a vacation, buying a new gadget, or building an emergency fund. Short-term goals are easier to achieve and give you quick wins. Here are some examples:

- Emergency Fund: Save at least three months of living expenses.

- Debt Repayment: Pay off high-interest debt such as credit card balances.

- Small Purchases: Save for a new phone or laptop.

Tracking your progress is crucial for achieving short-term goals. Use a budgeting app or a simple spreadsheet to monitor your savings.

Long-term Goals

Long-term goals take more time to achieve, usually five years or more. These goals require more planning and commitment. Examples of long-term goals include buying a house, saving for retirement, or funding your children’s education. Here are some examples:

- Home Purchase: Save for a down payment on a house.

- Retirement Savings: Invest in retirement accounts like 401(k) or IRA.

- Education Fund: Save for your child’s college education.

Long-term goals often involve investing. Diversify your investments to reduce risk and maximize returns. Consult a financial advisor for personalized advice.

Setting both short-term and long-term goals ensures a balanced financial plan. It keeps you focused and helps you achieve financial freedom.

Creating A Budget

Creating a budget is a crucial step in financial planning. It helps you understand where your money goes. It also aids in saving for future goals and avoiding debt. By tracking your income and expenses, you can make informed decisions.

Tracking Income And Expenses

Start by tracking your income. This includes salary, bonuses, and any other earnings. List all sources of income in a simple table:

| Source | Amount |

|---|---|

| Salary | $3,000 |

| Freelancing | $500 |

| Other | $200 |

Next, track your expenses. Divide them into categories like housing, food, and entertainment. Use another table to list them:

| Category | Amount |

|---|---|

| Housing | $1,200 |

| Food | $400 |

| Entertainment | $150 |

Subtract your total expenses from your total income. This will show your disposable income. If your expenses are higher than your income, adjust your spending.

Tools And Apps For Budgeting

Various tools and apps can help you manage your budget. Some popular ones include:

- Mint: Tracks your spending and helps create a budget.

- YNAB (You Need A Budget): Focuses on giving every dollar a job.

- Personal Capital: Offers budgeting tools and investment tracking.

These apps provide user-friendly interfaces. They also offer useful features like alerts and visual charts. They can help you stay on track with your financial goals.

Consider using a spreadsheet for budgeting. It allows customization and flexibility. Google Sheets and Microsoft Excel are great options.

Building An Emergency Fund

Building an emergency fund is a crucial step in financial planning. This fund acts as a safety net for unexpected expenses like medical bills or car repairs. It helps you avoid debt and provides peace of mind.

How Much To Save

Knowing how much to save is important. Experts suggest saving at least three to six months’ worth of living expenses. This amount covers essentials like rent, groceries, and utilities.

To calculate this amount, list your monthly expenses. Here’s a simple table to help:

| Expense | Monthly Amount |

|---|---|

| Rent | $1,000 |

| Groceries | $300 |

| Utilities | $200 |

| Transport | $150 |

| Other | $150 |

| Total | $1,800 |

Multiply the total by three or six to find your target savings. For example, if your total expenses are $1,800 per month, you should aim to save between $5,400 and $10,800.

Where To Keep Your Fund

Choosing the right place to keep your emergency fund is essential. It should be accessible but not too easy to spend.

Here are some good options:

- Savings Account: A basic savings account is a good choice. It is accessible and earns some interest.

- Money Market Account: These accounts offer higher interest rates. They are also easily accessible.

- Certificates of Deposit (CDs): CDs offer higher returns but have fixed terms. Choose short-term CDs for better accessibility.

Avoid risky investments like stocks for your emergency fund. It should be safe and liquid.

Managing Debt

Managing debt is a crucial aspect of financial planning, especially for beginners. It helps in maintaining financial health and achieving long-term goals. Understanding the types of debt and strategies to pay them off is essential for effective debt management.

Types Of Debt

Not all debts are the same. Here are the main types:

- Secured Debt: This type of debt is backed by collateral. Examples include mortgages and auto loans.

- Unsecured Debt: This debt is not backed by collateral. Common examples are credit card debt and personal loans.

- Revolving Debt: It allows you to borrow up to a limit. Credit cards are the most common form.

- Installment Debt: This type involves regular payments over a period. Examples include student loans and mortgages.

Strategies For Paying Off Debt

Effective strategies can help you manage and pay off debt faster. Here are some popular methods:

- Debt Snowball Method: Focus on paying off the smallest debt first. Then move on to the next smallest.

- Debt Avalanche Method: Pay off the debt with the highest interest rate first. This saves money on interest.

- Consolidation: Combine multiple debts into a single payment. This can simplify managing payments.

- Balance Transfer: Transfer high-interest debt to a lower-interest account. This can reduce the amount paid in interest.

- Budgeting: Create a budget to track income and expenses. Allocate extra funds towards debt repayment.

Understanding the types of debt and using the right strategy can help you regain control of your finances. Make informed decisions and stay committed to your financial goals.

Credit: www.fincash.com

Investing Basics

Starting your financial journey can feel overwhelming. But learning the basics of investing is a great first step. This section breaks down the essentials to help you get started.

Types Of Investments

There are several types of investments to choose from. Each has its own characteristics and benefits.

- Stocks: Buying shares of a company. You own part of the company.

- Bonds: Lending money to the government or a company. You earn interest.

- Mutual Funds: A mix of stocks and bonds managed by professionals.

- Real Estate: Buying property to rent or sell for profit.

- ETFs: Exchange-traded funds. They trade like stocks but hold a mix of assets.

Risk And Return

Investing involves balancing risk and return. Higher returns often come with higher risks.

| Investment Type | Risk Level | Potential Return |

|---|---|---|

| Stocks | High | High |

| Bonds | Low to Medium | Low to Medium |

| Mutual Funds | Medium | Medium |

| Real Estate | Medium to High | Medium to High |

| ETFs | Medium | Medium |

Understanding the risk and return of each type helps you make better decisions. Consider your financial goals and risk tolerance before investing.

Retirement Planning

Retirement planning is essential for securing your future. It ensures you have enough money to live comfortably. Many people overlook this critical aspect of financial planning. Start early to maximize your savings and investments. Let’s explore the key elements of retirement planning.

Types Of Retirement Accounts

There are several types of retirement accounts to consider. Each offers unique benefits and tax advantages. Here are the most common options:

- 401(k): Offered by employers, often with matching contributions.

- IRA: Individual Retirement Accounts available to everyone.

- Roth IRA: Contributions are taxed, but withdrawals are tax-free.

- Pension Plans: Offered by some employers, providing a fixed monthly income.

How Much To Save For Retirement

Determining how much to save can be challenging. Follow these steps to estimate your needs:

- Calculate your expected annual expenses during retirement.

- Multiply this amount by the number of years you expect to be retired.

- Factor in inflation to ensure you maintain your purchasing power.

- Consider other income sources like Social Security or pensions.

Experts recommend saving at least 15% of your income. Start early to take advantage of compound interest. Adjust your savings rate as needed to reach your goals.

Here’s a simple table to illustrate the power of early savings:

| Age Started Saving | Monthly Contribution | Amount at Retirement (7% return) |

|---|---|---|

| 25 | $200 | $500,000 |

| 35 | $200 | $250,000 |

| 45 | $200 | $120,000 |

As you can see, starting early makes a significant difference. Take charge of your retirement planning today.

Protecting Your Finances

Starting your financial journey can be exciting and overwhelming. One crucial aspect to focus on is protecting your finances. Ensuring your money is safe and secure helps prevent potential losses and gives peace of mind.

Insurance Needs

Insurance acts as a safety net for unexpected events. It helps cover costs that can otherwise drain your savings. Here are essential types of insurance:

- Health Insurance: Covers medical expenses and protects against high medical costs.

- Car Insurance: Provides financial protection against accidents or theft.

- Home Insurance: Protects your home and belongings from damage or theft.

- Life Insurance: Offers financial support to your family if something happens to you.

Fraud Protection

Fraud can significantly impact your finances. Taking steps to protect yourself is vital. Consider these tips:

- Monitor Accounts: Regularly check your bank and credit card statements.

- Strong Passwords: Use complex passwords and change them often.

- Secure Devices: Use antivirus software and keep your devices updated.

- Shred Documents: Destroy documents with personal information before discarding them.

- Be Skeptical: Avoid sharing personal information over the phone or online with unknown sources.

Taking these steps helps safeguard your money and personal information. Being proactive is key to maintaining financial security.

Seeking Professional Advice

Financial planning can be confusing for beginners. Seeking professional advice helps you stay on track. A financial advisor provides guidance tailored to your needs. Let’s explore when to hire one and how to choose the right advisor.

When To Hire A Financial Advisor

Hiring a financial advisor is beneficial at different life stages. Here are some scenarios:

- Starting a career: Advisors help you set goals and budget.

- Major life events: Marriage, buying a home, or having children.

- Inheriting money: They ensure you manage the inheritance wisely.

- Planning for retirement: Advisors help create a retirement plan.

- Complex financial situations: High income, investments, or business ownership.

How To Choose The Right Advisor

Choosing the right advisor is crucial. Here are some tips:

- Check qualifications: Look for credentials like CFP (Certified Financial Planner).

- Understand fees: Know how they charge – fee-only, commission, or a mix.

- Ask for referrals: Talk to friends or family who have used advisors.

- Interview potential advisors: Discuss your goals and see if they align.

- Check their experience: Ensure they have experience with clients like you.

Financial planning is a vital skill. Seeking professional advice can make the process smoother and more effective. Remember to hire a financial advisor when needed and choose the right one for your needs.

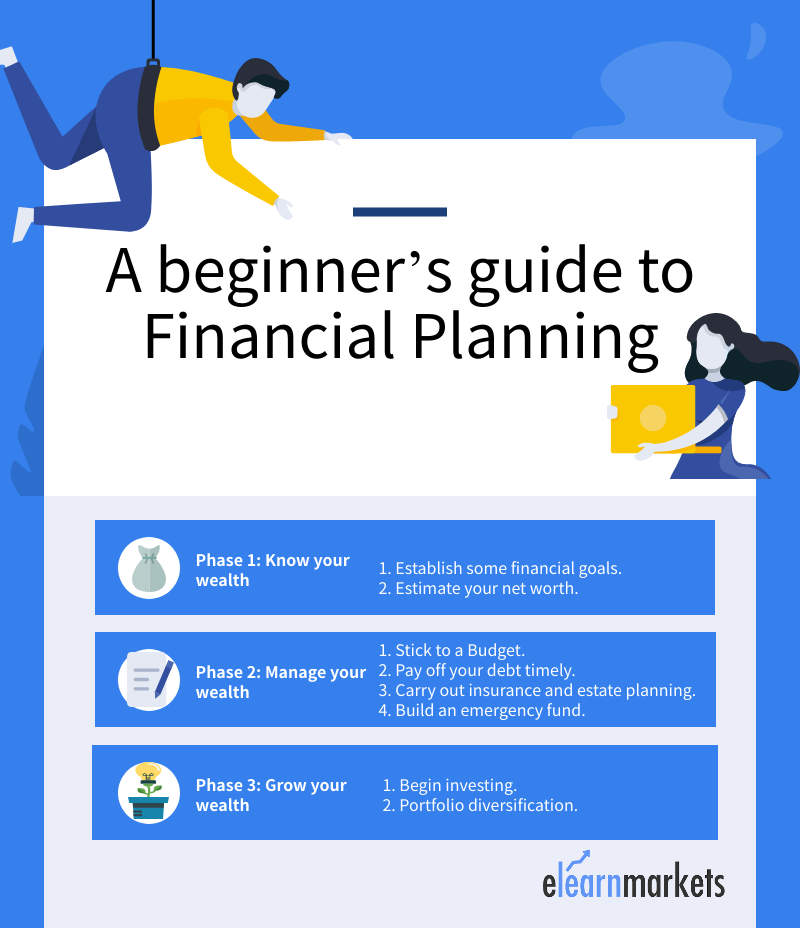

Credit: blog.elearnmarkets.com

Frequently Asked Questions

What Is Financial Planning For Beginners?

Financial planning for beginners involves creating a budget, saving, and setting financial goals. It helps manage money effectively.

How Do I Start Financial Planning?

Start by evaluating your income and expenses. Set realistic financial goals. Create a budget and stick to it.

Why Is Budgeting Important In Financial Planning?

Budgeting is crucial as it helps track income and expenses. It ensures you save and avoid unnecessary spending.

What Are The Key Steps In Financial Planning?

Key steps include setting financial goals, creating a budget, saving regularly, and investing wisely. Monitor and adjust as needed.

Conclusion

Starting your financial journey feels overwhelming. Small steps make a big difference. Understand your income and expenses. Set clear financial goals. Save regularly and invest wisely. Budgeting helps manage spending. Emergency funds are crucial. Avoid unnecessary debt. Seek advice when needed.

Stay disciplined and patient. Financial planning builds a secure future. Keep learning and adapting. Your financial health is worth the effort.